The Albanese government has, in the space of six weeks, abolished the 50% CGT discount, restricted negative gearing on established property, and, in a deal struck with the Greens on 23 June, agreed to ban new SMSF residential borrowing. This brief analyses what the data says, what the government is doing, and what it means for every stakeholder in Australian real estate.

The Inflation Picture: Don’t Be Fooled by Cheap Petrol

When the Australian Bureau of Statistics released the May 2026 CPI on 25 June, headline inflation appeared to fall to 4.0% — a number that made newspaper front pages look optimistic. The reality beneath it is the opposite of reassuring. Automotive fuel prices collapsed 11.9% in a single month — a combination of falling global crude prices and the government’s temporary fuel excise halving — dragging the headline figure down while doing nothing for the structural pressures consuming household budgets.

The Reserve Bank of Australia’s preferred measure, the trimmed mean, strips out these volatile price movements by design. It rose to 3.6% in the year to May 2026, up from 3.5% the previous month. This is the number the RBA Board actually targets for monetary policy, and it remains 0.6 percentage points above the top of the 2–3% target band.

KEY TAKEAWAY — THE “GOOD” HEADLINE NUMBER IS A MIRAGE

The RBA’s own May Statement on Monetary Policy projects underlying inflation will remain above 3% until late 2027, only returning to the 2.5% midpoint by mid-2028. The fight against inflation is far from over — and the sectors driving it are precisely those that define the cost of living for ordinary Australians.

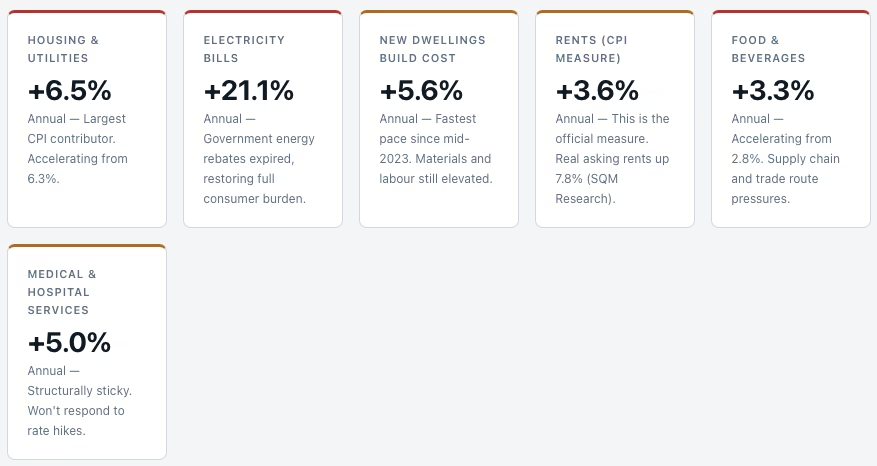

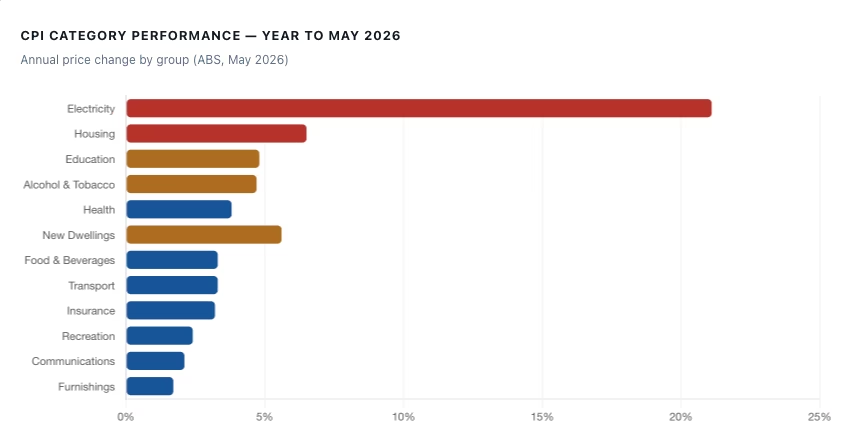

What Is Actually Driving Underlying Inflation

The data tells a clear story of entrenched domestic cost pressure. Three categories dominate:

What makes this inflation particularly difficult for the RBA to manage is its composition. The categories running hottest — housing, medical, education, insurance — are largely supply-constrained or structurally driven. Higher interest rates can suppress consumer spending but cannot build more houses, train more doctors, or reduce the cost of building materials. The RBA is fighting an enemy that doesn’t fully respond to its primary weapon.

The Rate Environment: Three Hikes in, Held in June — But Not Done

The RBA’s Monetary Policy Board voted unanimously to hold the cash rate at 4.35% at its June 2026 meeting — the first pause after three consecutive 25-basis-point increases earlier this year, fully reversing the 2025 easing cycle. Governor Michele Bullock confirmed that inflation remains the central concern and that the Board “will do what it considers necessary” to return it to target. A further hike cannot be ruled out.

“Inflation is still too high and remains a central concern for the Reserve Bank of Australia.”— RBA GOVERNOR MICHELE BULLOCK, JUNE 2026 PRESS CONFERENCE

The divergence between major bank forecasts reflects genuine uncertainty about the second-round effects of the Middle East conflict on energy costs and supply chains. What is agreed upon across all forecasters is this: rates will remain elevated for longer than previously expected, mortgage serviceability is under sustained pressure, and the era of 2-3% rates that inflated asset values throughout the 2020s is over for at least the next two years.

CBA’s own internal data shows consumers have remained relatively resilient in aggregate, but with “early signs of a pullback in spending in areas like travel and selected discretionary categories.” The RBA’s own May Statement on Monetary Policy projects headline inflation to peak at 4.8% in the June quarter 2026 under its baseline scenario, before gradually declining as rate tightening constrains demand.

💡 WHAT THIS MEANS FOR MORTGAGE HOLDERS

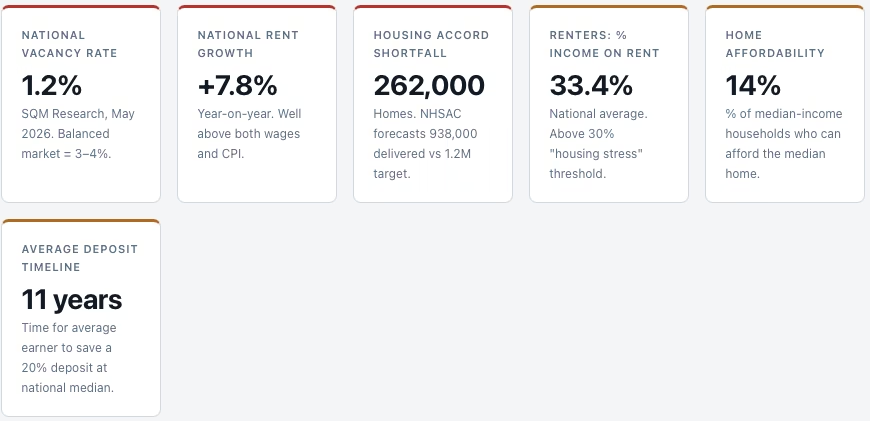

Australia’s national mortgage serviceability ratio has risen to 45.9% of gross household income — against a long-run average of 34.3%. A further 50bp in rate increases (Westpac scenario) would push this materially higher. Each 25bp RBA increase adds approximately $75/month to a $600,000 variable rate mortgage.

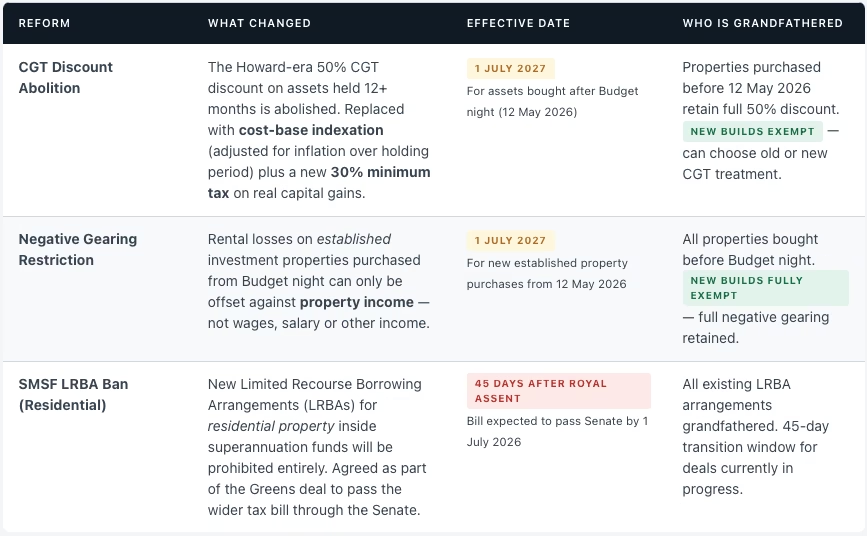

What the Government Has Done: The Biggest Tax Reset in 30 Years

The 2026–27 Federal Budget, handed down on 12 May 2026, represented the most significant intervention in Australia’s property tax framework since Paul Keating’s CGT regime in 1985. In the weeks since, additional measures have been layered on. Understanding the full architecture of change requires examining three distinct pillars.

The Three Policy Pillars

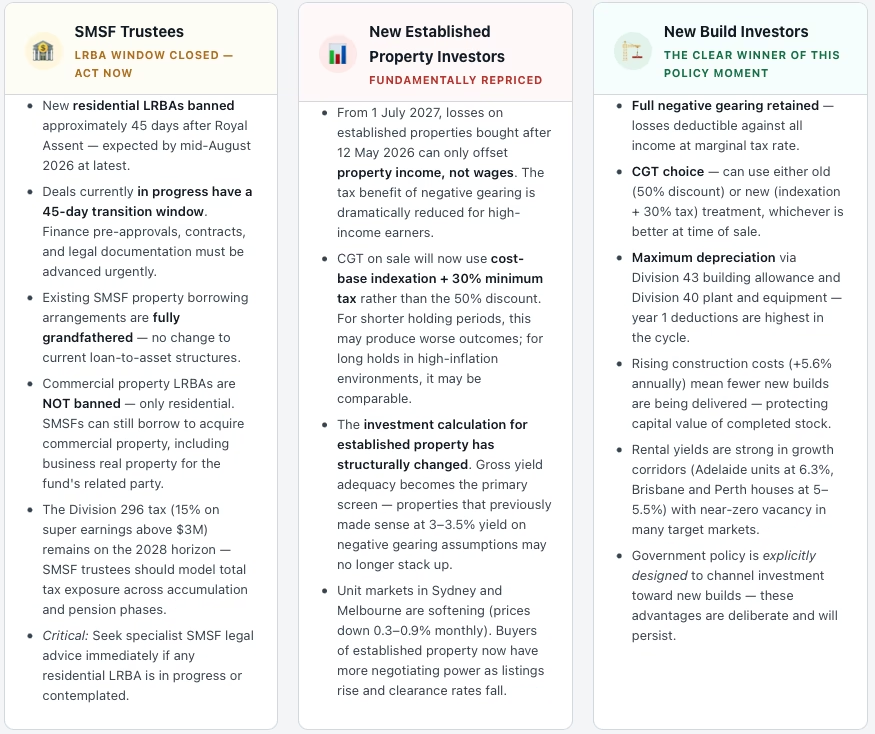

Why the LRBA Ban Matters — Even Though It’s “Small”

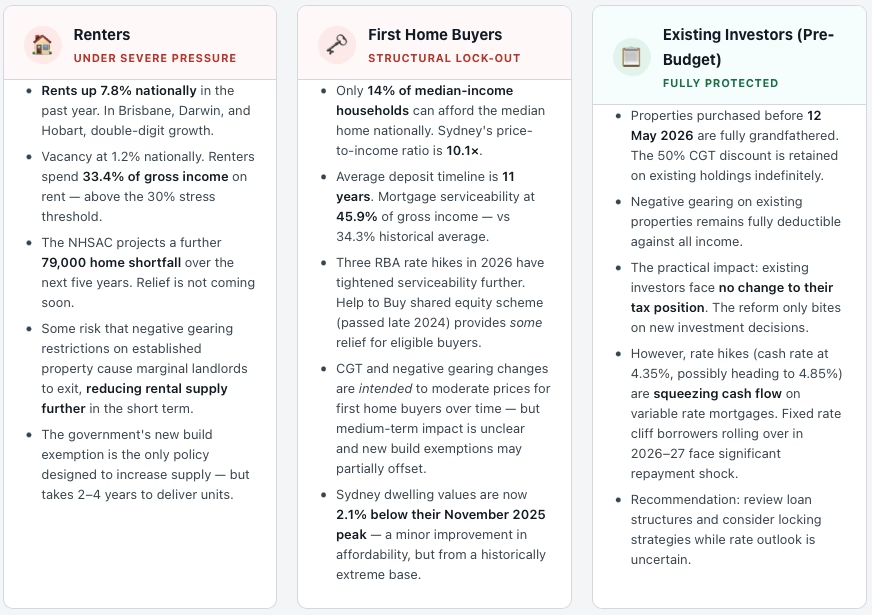

Treasurer Chalmers noted that SMSF residential borrowing represents less than 1% of total residential property borrowing. This is technically accurate. But the policy significance is disproportionate to the volume for several reasons. SMSF LRBAs were disproportionately used by high-net-worth investors to acquire new build property using concessionally-taxed superannuation capital — with an effective CGT rate of 10% on gains in accumulation phase and 0% for retirees in pension phase. The Greens’ stated concern was precisely that wealthy investors could use SMSFs to exploit the new build exemptions on CGT and negative gearing, effectively owning tax-advantaged investment property through a vehicle that compound advantages with superannuation’s concessional tax treatment.

The government explicitly linked the ban to the 2014 Murray Financial System Inquiry and warnings from the Council of Financial Regulators in 2019 and 2022 about leveraged exposure to residential property inside retirement savings vehicles.

⚖ THE GREENS DEAL — WHAT WAS AND WASN’T WON

The Greens secured: (1) the LRBA ban on residential property, and (2) removal of ministerial discretion to wind back CGT/negative gearing reforms. They did not win the scrapping of grandfathering — existing investors with properties purchased before Budget night retain full 50% CGT discount and unrestricted negative gearing. A second, more technical bill dealing with discretionary trust rules is due later in 2026.

The Policy Timeline

12 MAY 2026 — BUDGET NIGHT

CGT discount abolished; negative gearing restricted for new established property purchases

All properties purchased after this date subject to new rules from 1 July 2027. New builds explicitly carved out and remain fully exempt. This is the critical date line for every property investor’s purchase decision.

5 JUNE 2026

CGT and negative gearing bill passes the House of Representatives

First tranche of tax reform legislation cleared lower house. Senate passage pending Greens deal.

18 JUNE 2026

Small business CGT threshold raised to $10M turnover (from $2M)

A carve-out benefiting small commercial property and business owners. Startup CGT concession also announced.

23 JUNE 2026

Government agrees with the Greens to ban new SMSF residential LRBAs

45-day transition window from Royal Assent. Existing arrangements grandfathered. Bill expected to pass Senate by end of first week of July 2026.

1 JULY 2027

CGT and negative gearing new rules take effect

Cost-base indexation replaces 50% discount; 30% minimum CGT tax on real gains; negative gearing losses on established property ringfenced to property income only.

LATE 2026 / 2027

Second bill: discretionary trust and detailed carve-out rules

Technical legislation spelling out trust treatment, carry-forward rules, and investment structure exemptions. This is the piece that will resolve remaining ambiguity for family trust and company-held portfolios.

What Happens to Australian Real Estate: The Data and the Verdict

Where Prices Are Now

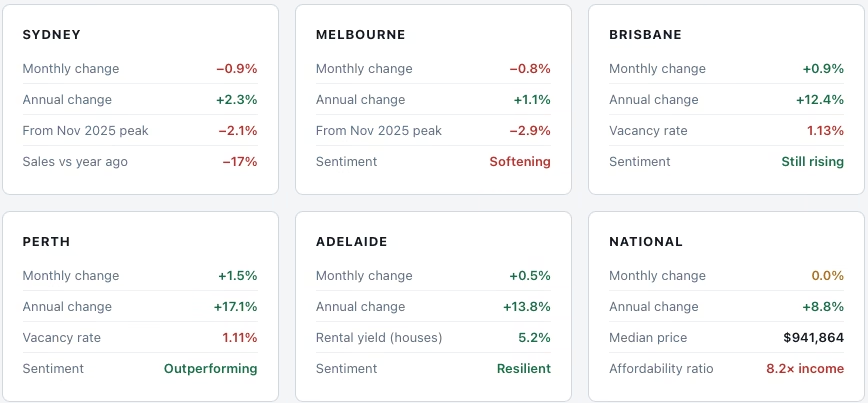

According to Cotality’s (formerly CoreLogic) Home Value Index released 1 June 2026, national dwelling values were flat in May— the weakest monthly result in a year. Annual growth sits at 8.8%, still reflecting the 2025 run-up, but the trajectory is turning. Sydney and Melbourne are leading the deterioration. The national median dwelling price now sits at $941,864, with the combined capitals median at $1,030,973.

The Rental Crisis: A Market in Structural Crisis

Australia’s rental crisis is not cyclical. It is structural. The national vacancy rate sits at 1.2% (SQM Research, May 2026) — roughly one-third of the 3–4% level that constitutes a “balanced” market. National advertised rents are up 7.8% year-on-year, and in cities like Darwin, Hobart, and Brisbane, double-digit annual rent growth is being recorded. Perth and Brisbane both sit below 1% vacancy — a level that in any credible reading of market dynamics means landlords have near-total pricing power.

🏗 THE NEW BUILD ADVANTAGE IS NOW STRUCTURAL — NOT JUST TAX-BASED

New builds retain full negative gearing, can choose between old CGT treatment (50% discount) and new treatment (indexation + 30% minimum tax), are ineligible for the established property restrictions, and command the highest depreciation claims. Combined with +5.6% annual construction cost inflation limiting new supply, new house and land packages have become the rarest and most advantaged investment vehicle in the Australian property market. The government’s own policy architecture has made them so.

Impact by Stakeholder: Who Wins, Who Loses, Who Must Act

The Price Outlook in Plain Terms

Cotality’s national outlook is for a “softer landing rather than a sharp downturn” — national values drifting sideways to mildly lower, with Sydney and Melbourne leading the softness while Perth, Brisbane, and Adelaide remain in positive territory but decelerating. This is the central scenario. The downside scenario (Westpac’s two further hikes) would accelerate Sydney and Melbourne declines into the 5–8% range from peak. The upside scenario (rate cuts in H1 2027, as CBA and NAB forecast) would stabilise and reverse softness in the large capitals.

What is not in doubt: the rental market will remain severely undersupplied regardless of what prices do. The 262,000-home shortfall against the National Housing Accord target, chronic construction cost inflation, and sustained population growth mean rents will remain elevated. The only market with structural relief in sight is new dwelling completions — and even those face 2–4 year delivery timelines.

The Verdict Panel

Five expert perspectives — macroeconomics, property markets, tax law, investment strategy, and housing policy — each delivering a direct verdict on the current environment.

1. MACROECONOMIST & RBA WATCHER

VERDICT: Inflation is the story everything else is a footnote to.

The 3.6% trimmed mean is not falling — it ticked up in May. The RBA has hiked three times and paused, but Governor Bullock has left the door open. Westpac’s two further hikes scenario is live. In that environment, saying the property market will hold up because of supply constraints is true but incomplete. Mortgage serviceability at 45.9% of gross income is already at a level that suppresses first home buyer entry and weakens investor appetite. Every further hike tightens the screw. Until trimmed mean falls convincingly toward 3.0%, the RBA’s bias is not toward easing. Property investors who are counting on cuts by mid-2027 are making a directional bet — and the data doesn’t fully support it yet.

INTEREST RATES: ON HOLD BUT NOT DONE

2. PROPERTY MARKET ANALYST (COTALITY DATA)

VERDICT: Two markets, not one. The national number is hiding a sharp divergence.

Sydney is 2.1% below its November peak and falling. Sales volumes are 17% below a year ago. Listings are rising. This is a buyer’s market in the large capitals and a seller’s market almost everywhere else. Perth and Darwin at 1.5% monthly growth while Sydney falls 0.9% in the same month — that’s not the same market. For investors, the unit sector nationally is outperforming houses because affordability pressures are driving renters and buyers down the price spectrum. The Budget changes and rate hikes have added weight to the second half of 2026. Do not extrapolate the national 8.8% annual figure — that’s 2025 momentum, not current trajectory.

NATIONAL PRICES: SIDEWAYS TO MILD CORRECTION

3. TAX LAW & SMSF

VERDICT: The LRBA window is closing in weeks. If you’re in progress, drop everything else.

The 45-day transition period sounds comfortable. It is not. Royal Assent is likely within days of Senate passage, which is projected for the first week of July. That gives SMSF trustees already in the pipeline approximately 45 days from that point — meaning LRBA finance must be unconditionally approved and documented before the deadline. Existing arrangements are safe. The commercial property LRBA exemption remains intact — a critical point that many advisers are missing in the noise. For clients with established SMSFs looking at residential property, the LRBA strategy is over. The pivot should now be toward residential property purchased outright within super, using contribution headroom and existing balances. On the CGT and negative gearing changes: the 1 July 2027 effective date gives established investors time to model scenarios, but the analysis should begin now, not next year.

SMSF LRBA: ACT WITHIN 45 DAYS OR NEVER

4. INVESTMENT STRATEGIST

VERDICT: New builds aren’t just preferred — they’re the only unconstrained game in town.

The government has explicitly structured the tax architecture to make new builds superior on every dimension: full negative gearing, CGT choice, maximum depreciation, no LRBA restriction. Combined with construction cost inflation suppressing supply delivery and rental vacancy at 1.2% nationally, the demand/supply equation for new build tenants is as favourable as it has ever been. Rental yields in Adelaide units at 6.3%, Brisbane houses at 5–5.5%, are approaching the point where properties cash flow positively at current rates — a rare condition in Australian residential investment. The ideal positioning right now: growth corridor new build house-and-land, strong tenant demand, holding structure that maximises depreciation and gearing, in a state where land tax treatment is manageable. Established property in Sydney or Melbourne without a compelling valuation discount is a hard case to make under the new regime.

NEW BUILDS: UNAMBIGUOUS STRUCTURAL ADVANTAGE

5. HOUSING POLICY

VERDICT: The government has changed investor incentives. It hasn’t solved the supply problem.

The most charitable reading of the Budget reforms is that they redirect investor capital toward new builds, which adds supply. The most sceptical reading is that restricting negative gearing on established property reduces the pool of rental supply without a sufficient replacement pipeline. Both readings have merit. The Housing Accord’s 262,000-home shortfall is not a political artefact — it’s structural, driven by construction labour shortages, planning delays, and the collapse in higher-density project feasibility when building costs are this high. The LRBA ban saves $50 million over the forward estimates. The housing shortage will cost Australian households hundreds of billions in rent and reduced productivity over the same period. The government is making ideologically coherent choices about who should own property. Whether those choices solve the housing crisis is a separate and largely unanswered question. Renters will not feel relief from this policy package for at least three to five years.

HOUSING SUPPLY: POLICY DIRECTS, MARKET DELIVERS SLOWLY

Disclaimer: This information has been prepared by Rishav Sinha for general educational and informational purposes only. It is not intended to provide, and should not be relied upon as, financial, taxation, legal, accounting, superannuation, or investment advice. While every effort has been made to ensure the accuracy of the information presented, data has been obtained from publicly available government, regulatory, and industry sources believed to be reliable as of 24 June 2026. No guarantee is provided regarding its completeness, accuracy, or ongoing validity. Property market performance, economic conditions, and legislative settings may change over time, and past performance is not a reliable indicator of future outcomes. Before making any property, investment, superannuation, taxation, or financial decisions, readers should seek independent advice from appropriately qualified and licensed professionals who can consider their individual circumstances and objectives.

Primary Sources: Australian Bureau of Statistics — May 2026 CPI Release | Reserve Bank of Australia — June 2026 Monetary Policy Decision & May Statement on Monetary Policy | Cotality (formerly CoreLogic) Home Value Index, 1 June 2026 | SQM Research — Residential Vacancy Rates, May 2026 | The Adviser — LRBA Ban Article, 23 June 2026 | National Housing Supply and Affordability Council (NHSAC) — Housing Accord Delivery Forecast | Demographia — Housing Affordability Survey 2025–26 | PropTrack / REA Group — Rental Vacancy Data | Westpac, CBA, NAB, ANZ Rate Forecasts — June 2026 | Treasury — 2026–27 Federal Budget Papers.