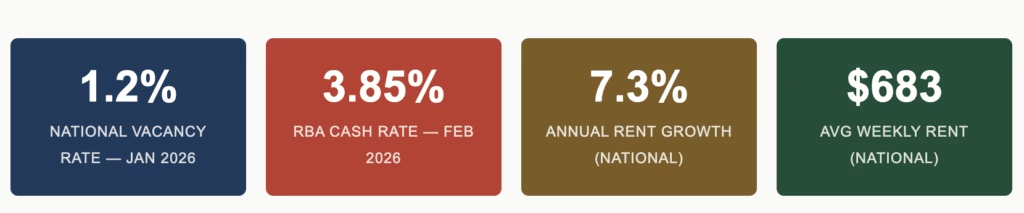

The national vacancy rate has collapsed to 1.2%. Rents are rising at 7.3% year-on-year. The RBA has just lifted the cash rate to 3.85%. Most investors are frozen, waiting for “the right time.” That’s exactly why a window is open right now — for those who know where to look.

The Headline Everyone’s Missing

When the Reserve Bank of Australia raised the cash rate to 3.85% in February 2026, the media did what it always does: sounded the alarm. Mortgage stress. Buyer exodus. Property crash looming. But the data tells an entirely different story — one that experienced investors understand well.

The same week rates went up, SQM Research released January vacancy data showing the national rental vacancy rate had dropped to 1.2% — a post-holiday tightening that reversed December’s seasonal lift in a matter of weeks. In absolute terms, just 37,630 dwellings are available for rent across the entire country. Brisbane sits at 0.9%. Perth at 0.6%. Darwin and Adelaide at 0.8%. Hobart, astonishingly, at just 0.4%.

These are not the numbers of a market in trouble. They are the numbers of a market in structural deficit — one where demand for rental accommodation is so far ahead of supply that higher borrowing costs are, at best, a minor headwind against a very powerful tailwind.

“The decline in the national vacancy rate to 1.2% in January highlights how quickly seasonal increases in rental supply can be absorbed in Australia’s current market. Unless we see a meaningful increase in new rental supply, upward pressure on rents is likely to persist through the first half of 2026.”— Sam Tate, Head of Property, SQM Research

Why Interest Rates Are Not the Whole Story

Here is the fundamental mistake most investors make in a rate-hiking cycle: they reduce a complex, multi-variable market to a single number — the cash rate — and make binary decisions based on it. In reality, the Australian property market in 2026 is being shaped by at least four forces that are all pulling prices upward, even as rates rise.

Structural undersupply. AMP’s chief economist Shane Oliver estimates Australia has an accumulated housing shortfall of 200,000 to 300,000 dwellings after years of under-building. The federal government’s target of 1.2 million new homes by mid-2029 is already more than 20% behind schedule after just 18 months. High construction costs mean many approved projects will never break ground. This is not a short-term dip in supply — it is a structural deficit that will take a decade or more to unwind.

Population growth. Net overseas migration remains elevated, with most new arrivals settling in Melbourne, Sydney, and Brisbane. Critically, only 38% of migrants own a home within five years of arriving — the vast majority rent. More people competing for a shrinking pool of available rental properties is a simple supply-and-demand equation that pushes rents — and by extension, property values — upward.

Government demand stimulus. The expanded First Home Guarantee scheme now allows buyers to purchase with a 5% deposit up to $1.5 million in Sydney. The Help to Buy scheme allows eligible Australians to purchase with the federal government contributing up to 30–40% of the property value. Both schemes add tens of thousands of new buyers to the market, increasing competition precisely in the segments — established homes and low-rise apartments — where investors typically compete.

Rising rents boosting investor yields. National advertised rents rose 2.2% in just the past 30 days and are 7.3% higher year-on-year. The national average weekly rent now sits at $683.26. Darwin leads annual rent growth at 9.4%, followed by Hobart at 10.1% and Brisbane at 8.5%. These rent increases are not just good news for existing investors — they are materially improving the yield maths for new ones, partially offsetting higher mortgage costs.

The City-by-City Picture: Where the Real Opportunities Are

Not all markets are equal. 2026 is emphatically a year of selective, not broad, opportunity. Below is the current vacancy and rent growth profile for every capital city, with investor signals attached.

| City | Vacancy Rate | Annual Rent Growth | KPMG Price Forecast | Signal |

|---|---|---|---|---|

| Darwin | 0.8% | +9.4% | +10%+ | High Conviction |

| Perth | 0.6% | +4.7% | +13% | High Conviction |

| Brisbane | 0.9% | +8.5% | +11% | High Conviction |

| Adelaide | 0.8% | +4.2% | +8.2% | Strong Watch |

| Hobart | 0.4% | +10.1% | +6% | Strong Watch |

| Sydney | 1.5% | +6.6% | +5.8% | Selective Only |

| Canberra | 1.4% | −1.0% | Stabilising | Wait and Watch |

| Melbourne | 1.7% | +5.2% | +6.8% | Selective Only |

The pattern is clear: the markets with the tightest vacancy rates are generating the strongest rent growth and are forecast to deliver the strongest capital growth in 2026. Perth, Brisbane, Darwin, and Adelaide are where the fundamentals are most compelling for investors right now. Sydney and Melbourne — while not falling — offer far less margin for error at their entry price points.

What Investors Should Actually Be Looking For

In a market where interest rates are elevated and growth is selective, the investment criteria that mattered less in the easy-money era of 2020–21 now matter enormously. Here is the framework smart investors are applying right now.

1. Lead With Yield, Not Just Growth

When borrowing costs are at 6–7% for investors, a property returning a gross yield of 3.5% requires significant capital growth just to break even. In 2026, yield is the foundation. Markets like Brisbane, Perth, Darwin, and select regional areas are generating gross yields of 4.5–7%+, which means the rent is doing real work to service the debt. The question to ask on any potential purchase is: can this property roughly cover itself at current rent levels? If the answer is yes, you have a far more resilient asset in a rate-volatile environment.

2. Focus on Units and Townhouses Over Detached Houses

The data consistently shows unit rents rising slightly faster than house rents in most capitals — a reflection of affordability pressures pushing more tenants toward medium-density housing. KPMG forecasts unit price growth of 7.1% nationally in 2026, nearly matching house growth, while units typically offer higher rental yields. For investors working with tighter borrowing capacity in 2026, a well-located unit or townhouse in an undersupplied suburb often delivers a better risk-adjusted return than a larger detached dwelling.

3. Look for the 20-Minute Neighbourhood

Post-pandemic, tenants and owner-occupiers alike will pay a meaningful premium for properties that allow them to live, work, and socialise within a 20-minute commute radius. The inner and middle-ring suburbs of Brisbane, Adelaide, and Perth — where gentrification is still in earlier stages than Sydney — represent areas where this premium has not yet been fully priced in. Investing ahead of amenity and infrastructure uplift in these zones has historically been one of the more reliable ways to generate above-average returns.

4. Prioritise Markets Where Local Income Is Growing

The single most important indicator of sustained rental demand and capital growth is whether local incomes are rising faster than the national average. Areas experiencing employment growth in high-income sectors — defence, healthcare, mining, technology — generate a tenant base that can afford rising rents without sacrificing quality. Darwin’s defence sector, Perth’s resources industry, and Brisbane’s infrastructure boom are all driving local income growth that underpins their rental markets.

5. Think in Decades, Not in Rate Cycles

Historical data is unambiguous on this point: Australian residential property has tripled in value in every 20-year block since World War II — meaning an average annual compound growth rate of roughly 6%. The investors who perform best over time are not the ones who perfectly time rate cycles. They are the ones who buy quality assets, in the right locations, with a holding period long enough for compounding to do its work. The rate cycle that feels definitive today will be a footnote in a decade.

What Investors Should Actually Be Doing Right Now

Get Your Finance Pre-Approved — Now

APRA is beginning to ramp up macroprudential controls. Borrowing capacity is tightening. The investors who move first on good assets are the ones who have their finance sorted before they start shopping. Use a broker who specialises in investment lending and understands debt-to-income ratios, offset structures, and interest-only periods.

Run the Cashflow Numbers Honestly

Calculate gross yield, net yield (after rates, insurance, strata, management), and your monthly holding cost after tax. Factor in a 1–2 vacancy week buffer per year. If the numbers work at a 7% interest rate, you have a genuinely robust investment. If they only work at 5.5%, you’re carrying rate risk that could hurt you.

Use Smart Loan Structures

In a high-rate environment, loan structure is as important as property selection. Interest-only periods reduce your monthly outgoing during the hold. Offset accounts provide liquidity without sacrificing deductibility. Fixed-rate tranches on a portion of the loan can provide cashflow certainty. Review your structure with your accountant and broker together, not separately.

Diversify Across Markets

Don’t concentrate all capital in one city. Spreading across two or three markets — say, a unit in Brisbane and a house in Adelaide — smooths your overall portfolio returns and reduces exposure to any one local market’s idiosyncrasies, including regulatory risks like Victoria’s expanded land tax regime.

Add Value Through Energy Efficiency

Tenants are increasingly factoring running costs into rental decisions. Properties with solar, batteries, heat pump hot water systems, and modern insulation command rental premiums and attract higher-quality, longer-term tenants. A $15,000–$25,000 investment in green upgrades can add more to rent and capital value than a full kitchen renovation.

Use Data Before Emotion

2026 rewards analytical investors, not emotional ones. Before any purchase, check the local vacancy rate trend (not just the current figure), the suburb’s rental yield history, population and employment drivers, infrastructure spending in the pipeline, and days on market. CoreLogic, SQM Research, and PropTrack all publish this data.

The Risks That Deserve Honest Attention

No investment strategy is without risk, and intellectual integrity requires acknowledging the headwinds as clearly as the tailwinds.

Key Risks to Monitor in 2026

Further rate rises: If inflation remains sticky above the RBA’s 2–3% target band, another rate hike cannot be ruled out. This would reduce borrowing capacity further and could dampen sentiment, particularly in Sydney and Melbourne where high entry prices make debt servicing tighter. AMP’s Shane Oliver notes that a “return to rate hikes could result in a resumption of property price falls.”

APRA tightening: The banking regulator is beginning to tighten investor lending conditions. Debt-to-income caps and higher serviceability buffers could reduce the borrowing capacity of highly leveraged investors faster than anticipated.

Slower migration: The federal government is actively reducing international student intake and temporary visa approvals. If net migration slows faster than expected, some of the structural rental demand underpinning tight vacancy rates could ease more quickly in certain markets.

Affordability limits: In Perth, Brisbane, and Adelaide, years of aggressive price growth are pushing median values toward Sydney-like affordability constraints. By mid-2026, analysts expect this to moderate growth in these previously fast-moving markets.

The Rentvesting Option: For Those Who Can’t Buy Where They Want to Live

One of the more compelling strategies gaining traction among younger investors in 2026 is rentvesting — renting where you want to live (often a city where you can’t afford to buy), while purchasing an investment property in a higher-yield, lower-entry-cost market. With Sydney house rents averaging $1,133 per week, and entry-level investment properties in Brisbane or Adelaide available for $550,000–$700,000 with yields of 5%+, the maths can work powerfully in favour of the rentvester. You capture capital growth and rental income in a strong market while maintaining lifestyle flexibility in your city of choice.

The Bottom Line for 2026

Australia’s rental market is not experiencing a cyclical tightening. It is experiencing a structural crisis of undersupply that is being intensified by population growth, a construction sector that cannot keep pace, and a decade-long backlog in housing delivery. Into this environment, the RBA has raised rates — which is real, and which matters, particularly for heavily leveraged portfolios. But rates are one variable in a complex equation. And right now, most of the other variables are pointing in the same direction for well-positioned property investors.

The investors who will look back at 2026 with satisfaction are not the ones who waited for rates to fall. They are the ones who ran the numbers honestly, found assets that could service themselves at today’s rates, focused on markets where demand demonstrably exceeded supply, and held on long enough for compounding to do its work.

The window is not wide. Investor activity is rebounding strongly — investor lending reached 38–40% of all new housing finance in early 2026, the highest share on record. Competition for quality assets in Brisbane, Perth, and Adelaide is already intensifying. The market waits for no one.

“2026 is shaping up to be a year of adjustment rather than a boom or a bust. This is good news for sellers and buyers — there will be both motivation and reassurance to make a move.”— Matthew Tiller, Head of Research, LJ Hooker

Your Next Move Starts Here: The data is clear. The markets are identified. The strategies are proven. What separates investors who build wealth in 2026 from those who watch from the sidelines is one thing — action.

Don’t wait for rates to fall. Don’t wait for prices to dip. Don’t wait for certainty that never comes.

Frequently Asked Questions

Should I invest in Australian property in 2026 despite rising interest rates?

Yes — but with a clear strategy. The structural fundamentals (1.2% national vacancy rate, 7.3% annual rent growth, 200,000–300,000 dwelling undersupply) support ongoing investor returns even as the RBA has lifted the cash rate to 3.85%. The key is choosing markets where the yield offsets higher borrowing costs and where long-term demand is structurally assured. Brisbane, Perth, Darwin, and Adelaide present the strongest case in 2026.

Which Australian cities have the tightest rental vacancy rates in 2026?

As of January 2026: Hobart 0.4%, Perth 0.6%, Darwin 0.8%, Adelaide 0.8%, Brisbane 0.9%, Canberra 1.4%, Sydney 1.5%, Melbourne 1.7%. Any market below 2% is considered tight. Australia’s average of 1.2% is among the tightest in the developed world.

What rental yield should I target in a high interest rate environment?

With investment mortgage rates typically sitting between 6–7%, investors should target a gross rental yield of at least 4.5–5% to minimise cashflow stress. A property returning 5%+ gross in a market with strong capital growth potential (like Brisbane or Perth) represents the most resilient combination in 2026. Below 4%, you are relying heavily on capital growth to make the numbers work — which adds meaningful risk if growth moderates.

Are Australian property prices expected to rise in 2026?

Yes, across most markets. KPMG forecasts national house price growth of 7.7% in 2026. Perth leads with approximately 13%, followed by Brisbane at 11% and Darwin at 10%+. Adelaide is forecast to grow around 8.2%, Sydney 5.8%, and Melbourne 6.8%. AMP’s Shane Oliver forecasts 5–7% national growth, down from 2025’s 8.6% result. The broad consensus points to continued but more moderate growth in 2026.

What is rentvesting and is it a good strategy in 2026?

Rentvesting means renting the property you live in — typically in a more expensive city — while purchasing investment property in a more affordable, higher-yield market. In 2026, it is a strong strategy for buyers who want to enter the market but can’t afford to buy where they live. A typical rentvesting scenario: renting in Sydney while owning an investment unit in Brisbane with a 5–5.5% yield, capturing capital growth in a stronger market while retaining lifestyle flexibility.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, tax, or legal advice. Property investment carries risk, including the potential loss of capital. Past performance is not indicative of future returns. Always seek advice from a qualified financial adviser, accountant, and licensed mortgage broker before making investment decisions. Figures sourced from publicly available research reports current as of February 2026.

Sources: SQM Research Vacancy Rate Data (January 2026) · KPMG Residential Property Outlook (January 2026) · AMP Investment Strategy, Dr Shane Oliver (February 2026) · Domain Property Forecast 2026 · LJ Hooker Research, Matthew Tiller · Propertyology Research, Simon Pressley · API Magazine, Lloyd Edge · Property Finance Invest · AUS Investment Properties